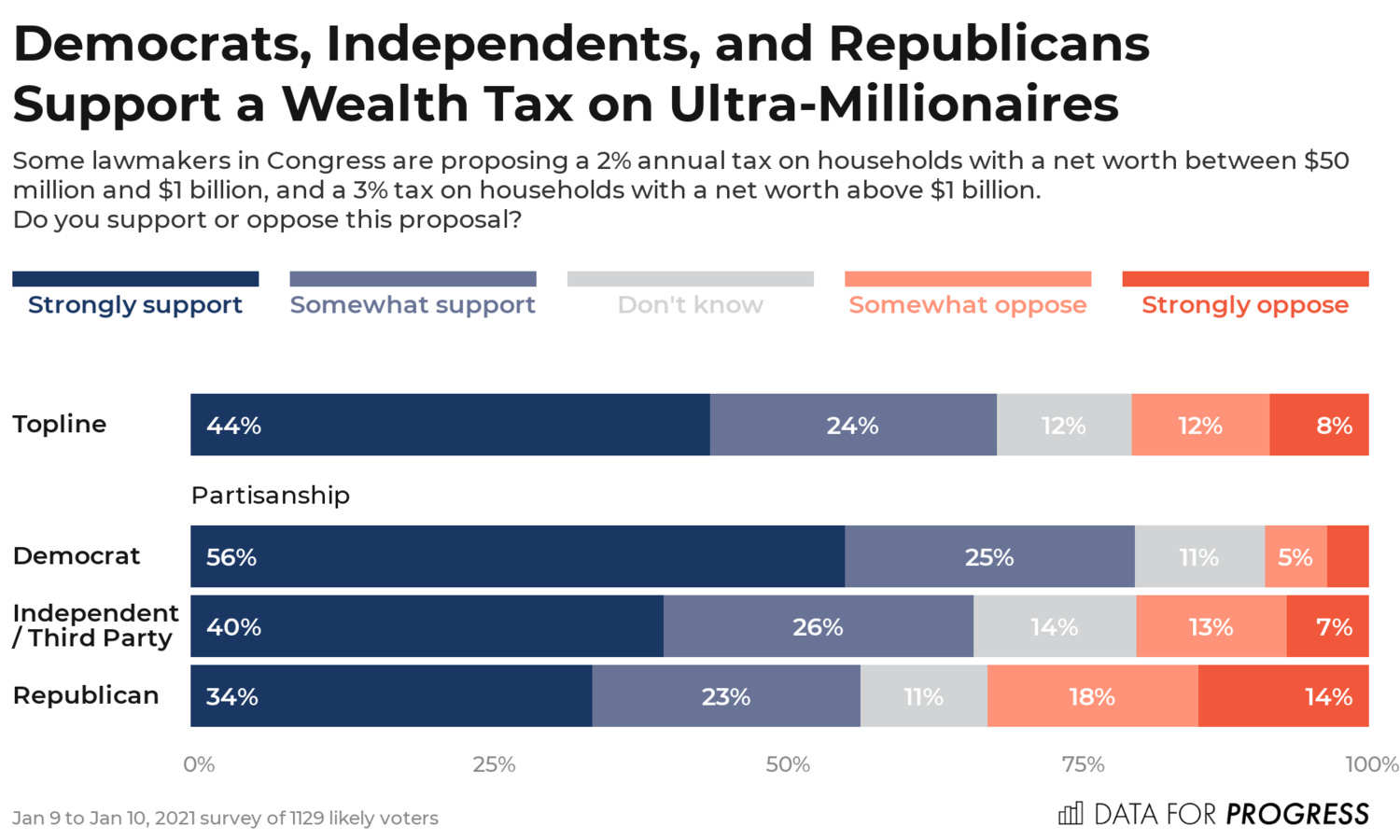

🤡 Happy April Fools Day! 👹 Today, I will discuss Adam Smith’s timeless answer to the following April-fools-like question: should the government impose a Bernie Sanders-style wealth tax on billionaires?

To see Smith’s answer to this query, we must turn our attention to Book V, Chapter 2, Part 2, Article 4 of The Wealth of Nations (available here; scroll down to “Article IV”), the fourth and final subsection of this monumental chapter, where the Scottish scholar surveys two types of taxes: “Capitation Taxes” (V.ii.j) and “Taxes upon Consumable Commodities” (V.ii.k). In today’s post, we will explore “capitation taxes”. What are they, and what does Adam Smith have to say about them?

In brief, a capitation tax is a direct “head tax” levied on each individual taxpayer, and such a tax can take one of two forms: it can either be fixed and uniform — i.e. every taxpayer owes the same amount of tax regardless of his level of income or overall wealth — or it can vary depending on a person’s wealth or social status. Either way, however, Adam Smith is highly critical of capitation taxes:

“Capitation taxes, if it is attempted to proportion them to the fortune or revenue of each contributor, become altogether arbitrary….

“Capitation taxes, if they are proportioned not to the supposed fortune, but to the rank of each contributor, become altogether unequal, the degrees of fortune being frequently unequal in the same degree of rank.

“Such taxes, therefore, if it is attempted to render them equal, become altogether arbitrary and uncertain, and if it is attempted to render them certain and not arbitrary, become altogether unequal. Let the tax be light or heavy, uncertainty is always a great grievance.” (WN, V.ii.j.2-4; my emphasis)

It’s fairly easy to see why a uniform or fixed capitation tax would be unfair and unequal in practice: people — even people in the same social class — are born with different talents and dispositions and are engaged in different activities and these diverse activities generate different levels of income. As a result, some people may not have the ability to pay a capitation tax, especially if the tax is set too high. But what about “variable” capitation taxes, i.e. a wealth tax that varies depending on the amount of a person’s overall wealth? Why, in short, would Adam Smith object to a wealth tax, even one that is “light” or modest? Simply put, because wealth taxes are uncertain and arbitrary:

“The state of a man’s fortune varies from day to day, and without an inquisition more intolerable than any tax, and renewed at least once every year, can only be guessed at. His assessment, therefore, must in most cases depend upon the good or bad humour of his assessors, and must, therefore, be altogether arbitrary and uncertain.” (WN, V.ii.j.2)

In other words, wealth taxes are a recipe for disaster. For starters, how would the government even begin to measure a person’s wealth? Depending on the composition of a person’s portfolio of economic assets (real property, stocks, bonds, etc.), one’s overall level of wealth is in constant flux — changing day by day, even hour by hour! This inherent uncertainty, in turn, would give tax officials way too much discretion — discretion that will ultimately end up being abused! Sorry Sam (Samuel Fleischacker), but Smith is not a “progressive” when it comes to wealth taxes.

Nota bene: We will proceed to taxes on consumption goods and conclude our survey of Chapter 2 of Book V of Smith’s magnum opus in my next two posts.