Today is Good Friday or “Viernes Santo” in Spanish, the most solemn day in the Catholic liturgical year.

In his survey of “Taxes upon Consumable Commodities” in Book V, Chapter 2, Part 2, Article 4 of The Wealth of Nations (WN, V.ii.k), Adam Smith explores the economics of crime — specifically the economics of smuggling. And in the course of his discussion of smuggling, Smith makes another timeless observation about the relative merits of excise taxes versus customs duties: simpler tax systems are better because they are more certain and more precise than complex tax systems are.

First off, recall from my previous post Smith’s timeless observation about the direct relationship between the level of taxes on consumption goods and the level of smuggling of those same goods. In short, it is “high taxes” that “encourag[es] smuggling” (V.ii.k.33); the higher those consumption taxes are, the more smuggling will occur. Next, the Scottish scholar identifies two ways of reducing smuggling:

“… it [the smuggling of consumption goods] may perhaps be remedied in two ways; either by diminishing the temptation to smuggle, or by increasing the difficulty of smuggling. The temptation to smuggle can be diminished only by the lowering of the tax, and the difficulty of smuggling can be increased only by establishing that system of administration which is most proper for preventing it.” (V.ii.k.35; my emphasis)

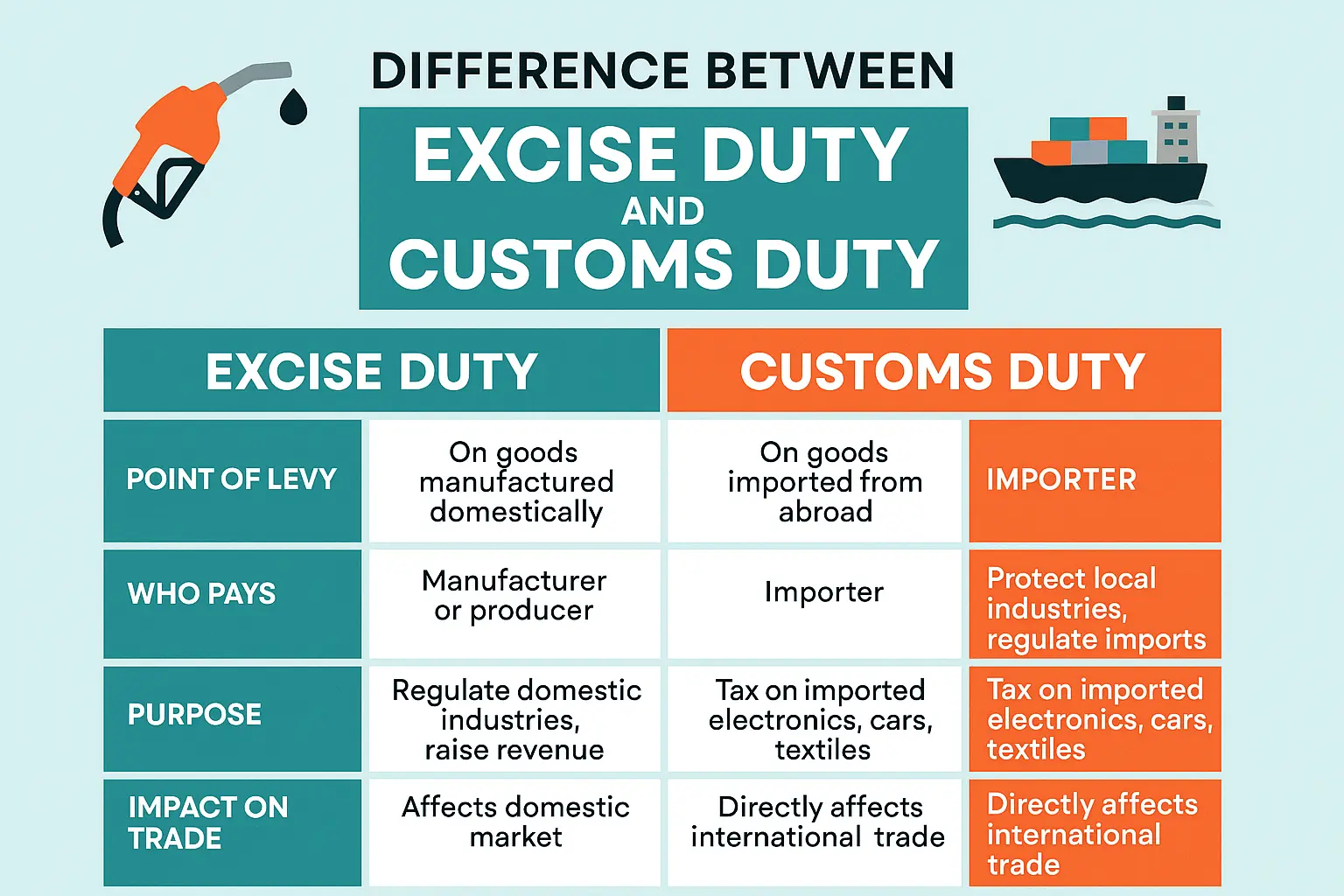

In other words, incentives matter! The government can reduce the level of smuggling by changing the incentive structure of smugglers in one of two ways: either by lowering the taxes on the goods being smuggled in (thus reducing the pecuniary temptation to smuggle in those goods in the first place) or by making it more difficult to evade detection. On this note, Smith explains why “[t]he excise laws … obstruct and embarrass the operations of the smuggler much more effectually than those of the customs.” (V.ii.k.36) Why? For Smith, there are three reasons why excise taxes > customs duties: “simplicity, certainty, and precision.” (cf. V.ii.k.38)

According to Smith, excise taxes are more simple, certain, and precise than customs duties because excise taxes are imposed on all designated goods produced or sold domestically, while customs duties are levied only on goods crossing international borders (imports or exports, or both). In other words, trying to figure out which goods are meant for export and which goods are imports is more costly and cumbersome than trying to figure out which goods were produced or sold in the home market. (In addition, custom duties are easier to evade than excise taxes are because custom duties are collected only at designated border checkpoints, which smugglers can find ways of bypassing, while excise taxes are collected at the point of production, distribution, or sale, depending on how the excise tax is designed.)

More importantly, Adam Smith then concludes his discussion of smuggling with the following general observations:

“… if every duty was occasionally either heightened or lowered according as it was most likely, either the one way or the other, to afford the greatest revenue to the state, taxation being always employed as an instrument of revenue and never of monopoly, it seems not improbable that a revenue at least equal to the present net revenue of the customs might be drawn from duties upon the importation of only a few sorts of goods of the most general use and consumption, and that the duties of customs might thus be brought to the same degree of simplicity, certainty, and precision as those of excise.” (V.ii.k.38; my emphasis)

In plain English, in the above passage Smith is making the following points:

- The purpose of taxation is to raise revenue, not to favor one lobby group over another (e.g. farmers, homeowners, etc.), a lesson that, alas, has clearly been lost on us today.

- Sometimes the government can collect more tax revenue by lowering tax rates. (See also Part B of my previous post.)

- Excise taxes (e.g. sales taxes) are more simple, certain, and precise than customs duties.

Nota bene: I will conclude my survey of Article 3 of Part 2, Ch. 2, Book V of The Wealth of Nations in my next post.