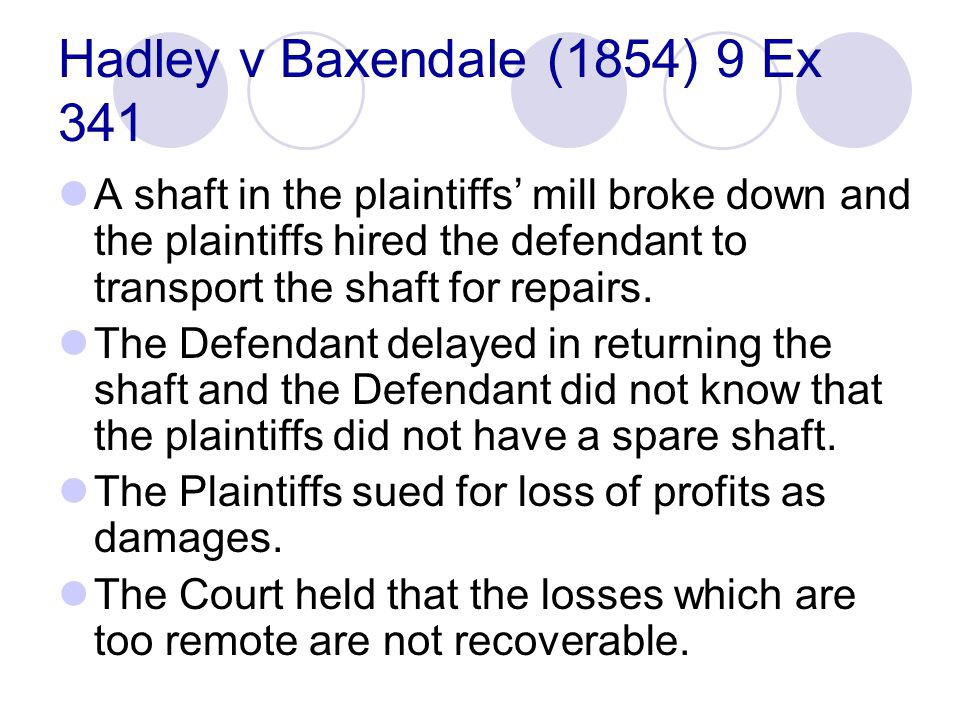

Updated Nov. 15 & 20 (see “Notes” below). We recently presented a “Bayesian defense” of the famous legal rule in Hadley v. Baxendale at the 2017 meeting of the Southeastern Academy of Legal Studies in Business (SEALSB). (Our talk was based on our forthcoming paper to be published in the FSU Law Review.) The facts of this great case are restated in the image below, but our argument does not dwell so much on the material world of broken crankshafts and idle grain mills; instead, we begin by posing the following theoretical question: if self-interested and rational actors were to choose a remedial contract rule from behind a veil of ignorance, what type of contract remedy or rule would such imaginary envoys agree to in the original position?

First, let’s consider three possible remedial rules to choose from. On one extreme, we can envision a rule of “total liability”, i.e. a pro-victim remedial rule in which breaching promisors are always liable for all losses flowing from their breaches of contract, no matter how remote or unforeseeable such losses might be. On the other extreme, we can image a rule of “zero liability”, i.e. a pro-breacher rule in which promisors are never liable for any losses resulting from their breaches. Lastly, between these extremes, we can imagine a “moderate liability” rule like the one in Hadley v. Baxendale. (For the record, the rule in Hadley is usually stated in terms of “reasonable foreseeability.” In brief, a breaching party is legally liable only for foreseeable losses, i.e. economic losses that were reasonably foreseeable at the time the parties entered into their contract.) So, which of these three rules would we choose in the original position?

Notice that, although my question is a Rawlsian one, John Rawls’ famous theory of justice is of no help here. Why not? Because once we leave behind the original position, we will most likely assume with equal frequency both contract roles of promisor (a party who makes promises) and promisee (a party who receives promises). Given this premise, we would apply an “equiprobability model” to our initial question. That is, when there is no reason to assign a greater likelihood to one alternative rather than another, then an equal probability should be assigned to each potential outcome. By way of example, let’s say that you are in the original position, so you don’t know whether you will be assigned the role of promisor or promisee in a particular breach-of-contract case. Your decision problem boils down to this: what liability rule should you choose in this ex ante situation: (a) zero liability, (b) the Hadley rule, or (c) total liability? To make this decision problem tractable, I will assume that potential promisors and potential promisees are Bayesian, and I will also make the following additional simplifying assumptions:

-

- TOTAL LIABILITY: You will be awarded $100,000 for your losses in the event of breach if you are the promisee, and you will have to pay out $100,000 in the event of breach if you are the promisor;

- HADLEY RULE: You will receive x for your losses in the event of breach if you are the promisee, and you will have to pay out x in the event of breach if you are the promisor, where x is between 0 and $100,000;

- ZERO LIABILITY: You will receive 0 for your losses in the event of breach if you are the promisee, and you will have to pay out 0 in the event of breach if you are the promisor.

As a result, since there is an equal probability you will be assigned either the role of promisor or the role of promisee in the original position (i.e. pp’ee = .5 and pp’or = .5), the expected value of the best outcome for you in the role of promisor is +$50,000 and the expected value of the worst outcome for you in the role of promisee is –$50,000. Given this setup, we can now reframe our original question about contract remedies as follows: (1) would you prefer to be awarded a lottery ticket that had a .5 probability of rewarding you $50,000 and a .5 probability of penalizing you $50,000, or (2) would you prefer to pay a definite amount of cash equal to x to avoid getting this lottery ticket? In other words, how much would you be willing to pay to avoid having to choose the lottery ticket? Even though the expected value of the lottery ticket described above is 0, my claim is that most people would be willing to pay some small sum to avoid being awarded such a lottery ticket. If my claim is correct, the reasonable foreseeability rule in Hadley might make the most sense from a Bayesian perspective.

Note #1 (11/15): One’s decision regarding whether to accept the lottery ticket or whether to pay $x to avoid the lottery ticket probably depends in great part on how small or large x is. The smaller x is, the more likely one would prefer the certainty of paying x to a .5 probability of being a promisor under a rule of total liability.

Note #2 (11/20): In recent correspondence with Zilu Wang, a student at the University of Rochester, I now realize that Harsanyi’s approach to decision-making can be extended to ethical dilemmas like the Trolley Problem. (There are, in fact, two different trolley problems!) Simply put, one could reframe the life-or-death decision in either version of the Trolley Problem as a negative lottery and then ask how much one would be willing pay to avoid playing this lottery. This possibility warrants a separate blog post and an update to our 2014 Drake Law Review paper “Trolley Problems,” so stay tuned. We will report back soon.

Credit: Lee Swee Seng

Pingback: A Bayesian approach to the trolley problem? (mini-thought experiment) | prior probability