I outlined my proposal for a “truth market” in my previous post. A truth market would trade in belief contracts. Each belief contract would be structured as a simple “belief statement” with two discrete choices: True(T) or False(F). The belief statement could refer to a disputed news story (e.g. fake news) or to a popular or persistent conspiracy theory. Consider, for example, the many conspiracy theories regarding the assassination of President John F. Kennedy on November 22, 1963. Was there a conspiracy to assassinate President Kennedy, or did Lee Harvey Oswald act alone?

If there were a truth market, anyone could post a belief statement such as “Lee Harvey Oswald was part of a conspiracy to assassinate JFK.” In the alternative, the belief statement could be more specific: “The Secret Service was part of a conspiracy to assassinate JFK” or “Fidel Castro ordered the assassination of JFK.” The creative possibilities are endless (see here, for example), but to keep it simple, let’s stick with the first example: “Lee Harvey Oswald was part of a conspiracy to assassinate JFK.” People who believe that Oswald did not act alone–that he was, in fact, a member of an anti-Kennedy conspiracy–could buy T contracts. Conversely, people who believe the official version (e.g. the Warren Commission’s lone gunman theory) could buy F contracts.

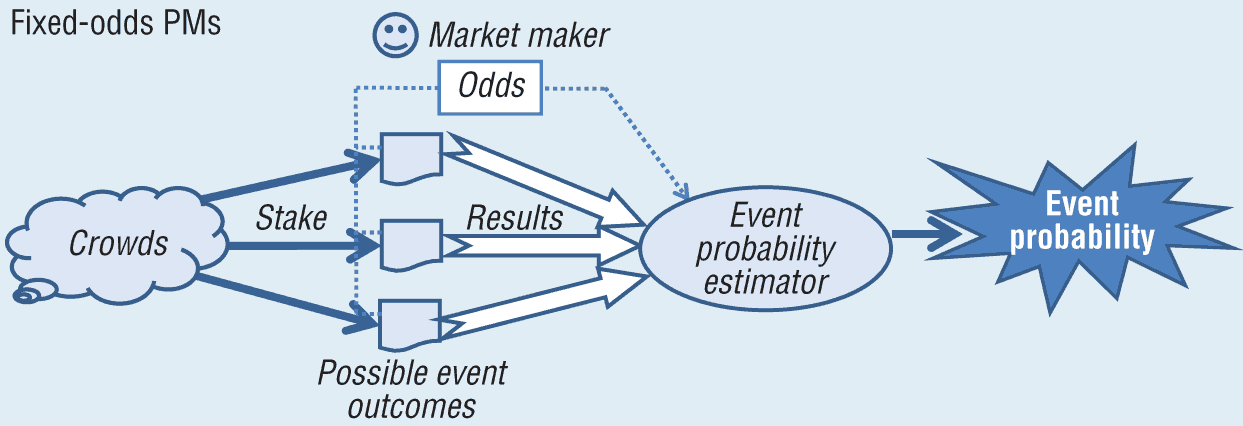

In a well-functioning truth market, the price of each belief contract (T or F) should reflect the betting market’s aggregate answer to the belief or conspiracy theory being bet on–i.e., whether the belief in the JFK conspiracy will turn out to be more likely true or false. (See, e.g., Wolfers & Zitzewitz, Interpreting prediction market prices as probabilities, NBER Working Paper #12200 (April 2006) For a less technical explanation, see here.) If more bettors are convinced that Oswald was part of a conspiracy, the price of a T contract will rise; by contrast, if more bettors believe that Oswald acted alone, the price of an F contract will rise. Either way, anyone who disagrees with the current consensus about a disputed conspiracy theory or disputed news story would have a profit motive to participate in the market.

But what about liquidity? Would people want to bet on conspiracy theories or fake news? Alas, without a sufficient number of market participants, it is less likely that the prices of these belief contracts will reflect the true probabilities of the various beliefs being bet on. Also, even if my truth market were highly liquid, with lots of bettors, one could argue that the truth of X belief should not depend on the number of people who are willing to bet on that belief.

Accordingly, next week I will address this crucial objection and propose some ideas for making truth markets more appealing to actual bettors.

Do you think that some application of the central limit theorem could in part suggest why we get closer to the truth when we get feedback from multitude of sources rather than centralized source?

I hadn’t thought of that but yes, I will pursue that avenue!

Pingback: Truth market feedback | prior probability

Pingback: Schraub’s critique of my truth markets idea | prior probability

Pingback: A modest proposal (JFK truth market edition) | prior probability

Pingback: Liquid truth markets | prior probability